US Economy Embraces 100 Oil Price Shock

Overview

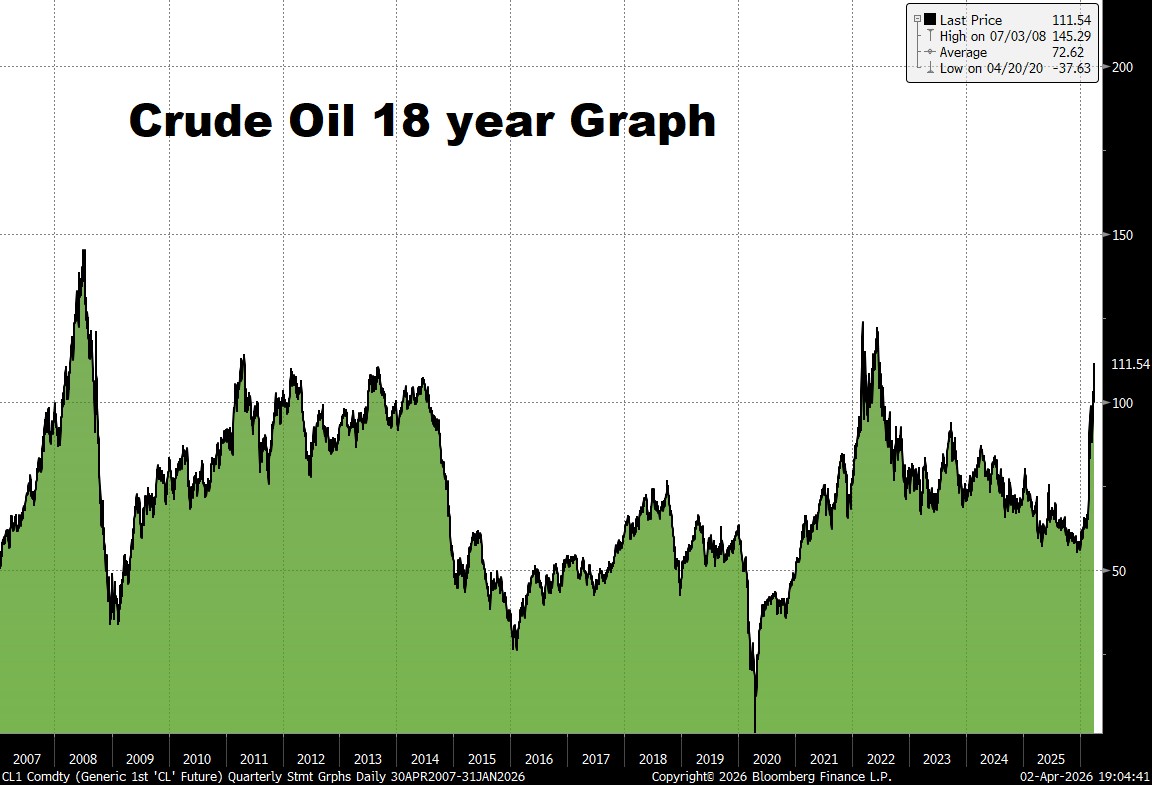

The US economy continues to grow despite geopolitical events and the shock of oil surging over $100 per barrel. The US economy has been in growth mode since the 2020 Covid led recession. Economists and market strategists have continued to expect a recession but without visible rot in the economy and with an abundance of jobs and steady improvement in personal income, the economy stays on course. The first quarter was full of changing expectations for inflation, interest rates, and growth. At the beginning of the quarter economists thought sure a recession would emerge, but by mid-quarter those fears had diminished as strong employment and steady consumption continued in America. By the end of the quarter war with Iran had begun and the price of oil suddenly surged over $100 a barrel. (Figure 1). The straight of Hormuz was closed and the extent of the closure has created vast uncertainty about the price of oil and inflationary fears surged again. As a result, interest rates on treasuries rose over 50 basis points from 3.70 to 4.40 for the 10 year treasury. Equity investors at first shrugged her shoulders about a possible recession but by the end of the quarter investors began to sell stocks and markets were down with most equities losing 4 to 8% and bonds declining 1 to 2% during the quarter. MACM’s dynamic growth portfolio lost 2.7%. The markets suffered their first quarterly loss since the first quarter of 2025. Consumer confidence was surprisingly strong even as the war grew more intense and Trump threatened to obliterate Iran and return it to the Stone Age.

Economic Review Q1 2026

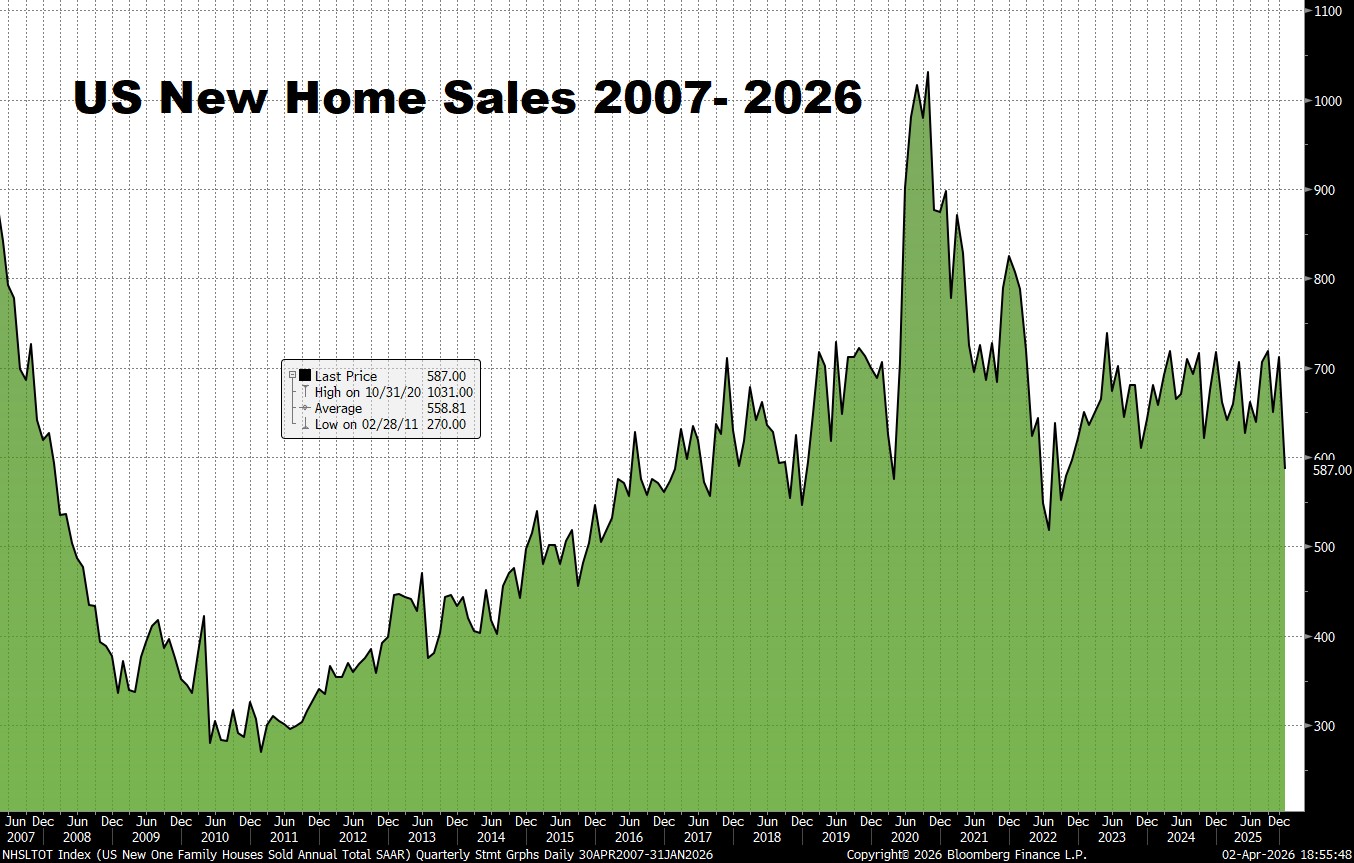

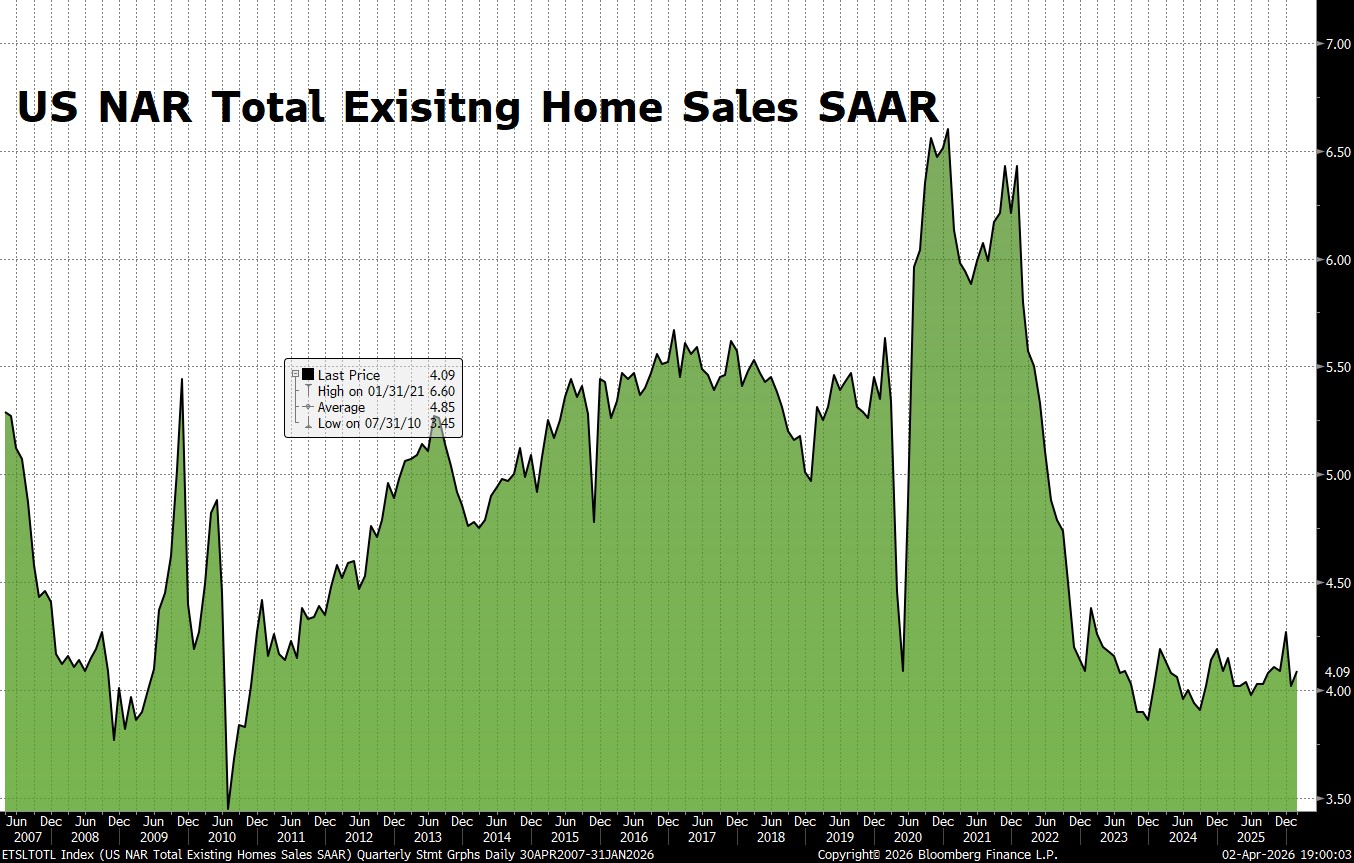

The US economy did well in the first quarter and we even began to see recovery in the industrial sector where manufacturing has been in recession for over two years. The service sector remained strong and robust growth was notable. The purchasing manager’s survey showed the sector to be expanding for the first time in over eight quarters. The Purchasing manager’s survey showed the NAPM PMI numbers to be at 52.4 and rising which is indicative of an expansion in the manufacturing sector. This is surprising because Interest rates unfortunately are now back at the high-end of the range they have seen for the last two years and this will certainly put a dent in the already soft housing sector. Housing continues to be the area of concern for the US economy. Both existing home sales (figure 2) and new home sales (figure 3) are way below levels considered to be consistent with a good economic cycle. New home sales have declined from over 700,000 per month to approximately 600,000 per month over the last several months. Consumers have been unwilling to sell their homes give up their 2 to 3% mortgages so the turnover in housing has been minimal. This is affecting homebuilders as well as home supply companies like Lowe’s and Home Depot.

The bright spot in the economy continues to be employment where unemployment has been steady at 4-4 ½% for some time. There is very little overcapacity in the economy and while there have been some layoffs in the tech sector and e-commerce sectors it is not tied to any significant downturn but merely corporate America adjusting their workforce to what is needed in their highly productive technologically driven systems. The jolts numbers which measures available jobs held steady at around 7000 and has been at that number for over one year. Wages for US employees continue to rise at or above the inflation rate. This is supportive to the strength that we have seen in retail sales and personal consumption. While consumers continue to complain about everything they continue to spend at an above trend pace.

When we look at the economy and worry about recession we certainly have to look for rot that might bring the economy to its knees. The sort of rot that is troublesome involves overcapacity, excess amounts of debt, or extremely overextended consumers. This is simply not visible in our economy today. Earnings growth for the S&P 500 came in at over 12% for everything that reported in the first quarter. This was surprisingly good. GDP which is bumpy unexpectedly slowed to less than 1% in the quarter after a strong previous quarter that was above expectations.

Financial Market Review

The equity market fell in the first quarter as investors optimism for continued earnings growth declined understandably as the war intensified and the price of oil pushed above $100 a barrel. While energy prices are not the most important driver of consumption they can’t be ignored given the already high level of prices we have in our economy. The Inflation that we saw in 2022 and 2023 is gradually being absorbed by consumers but the higher energy prices threaten the consumers ability and confidence to continue to spend at a trend like pace.

There were some areas of the equity markets that did well. Energy, chemicals, gas, and industrials all had strong positive returns in the quarter. Expectations fell for artificial intelligence, software, healthcare, travel, and consumer discretionary items.

The equities that declined the most involved the Russell 1000 growth which was off 9.8%. The Russell 1000 value Index advanced 2% while the S&P 500 declined 4.3%. The energy sector had a terrific quarter as oil advanced. Energy stocks were up over 35%. Commodities and basic materials also had great quarters. Financials, consumer discretionary areas and technology fell 7-9% during the quarter. The magnificent seven was also weak declining over 12%. MACM dynamic growth portfolio fell 2.7%. There was no safe haven in foreign mature markets. Europe had similar declines as America and China fell over 6%. Emerging markets did a bit better and advanced 2 to 4% in the quarter. Mexico did extremely well with the EWW gaining over 8% as investors grew optimistic that the business lost in China because of the trade war would be captured by Mexican manufacturers.

Fixed income markets were mostly flat to lower. Bitcoin declined over 22% during the quarter and continued a losing streak that has been ongoing for several quarters. Gold advanced 8 ½%, and silver gained over 5%.

Real estate investment trust had a mixed quarter. Residential property was flat to slightly higher. Similar performance was seen in retail properties and malls. However, office buildings continue to see tenants leave and occupancies are averaging about 60% nationwide down from over 95% pre-covid. Office properties lost over 20% in the quarter.

Economic Outlook

Until the war is over the outlook for economic growth is a bit uncertain. It’s hard to bet against the current trend which is steady consumption and steady growth. Earnings growth is expected to exceed 13% in this quarter for the S&P 500. GDP is expected to grow at over 2% in this quarter and advance to 4% or more in the following quarter. This will be good for equities.

There are several Consumption themes in place that will continue – AI, entertainment and leisure, Web Computing, Digitization of data, Ecommerce, Electric Vehicles, Robots, and Solar. There certainly are challenged areas of the economy that include healthcare durable good manufacturing housing and selective drugs. The level of prices in the economy is still a problem but consumers are gradually adapting.

Financial Market Outlook.

We believe Equities are better positioned than other risks Assets, however equities may continue to underperform until the impact and extent of the war is more certain. Fixed income will not be a haven as rates will rise further if oil stays above $100. The closure of the straight of Hormuz is the only reason why this war is a problem for the markets. Investors have generally decided that most of these conflicts in the world are not meaningful to the global economy. However, Iran sits on the border of a narrow 20 mile straight that 20% of the oil reserves in the world passes through every day. Washington has been putting patches on this problem with Iran for 40 years and it could be that we are done kicking the can down the road and will move to eliminate Iran leadership and make the world a safer place and ensure that oil can pass from the gulf safely every day. It is unclear what Trump will do.

It seems like the recovery in the manufacturing sector is real and we will continue to increase our exposure to industrials and manufacturing companies that will benefit from this change of trend. We are already overweight industrials. We believe emerging markets will continue to benefit from an improvement in the manufacturing sector and we have already taken a position in emerging markets which we plan to increase. We will continue to avoid small-cap stocks until there is more signs that above trend growth is possible in this world of high prices. We believe that travel and leisure, artificial intelligence, and obesity are strong consumption themes that will continue and the companies surrounding them will benefit and we will continue to be overweighted in this group.

We remain optimistic

Figure 1

Figure 2

Figure 3