Month: July 2026

Lower Oil Prices but Higher Chip Prices

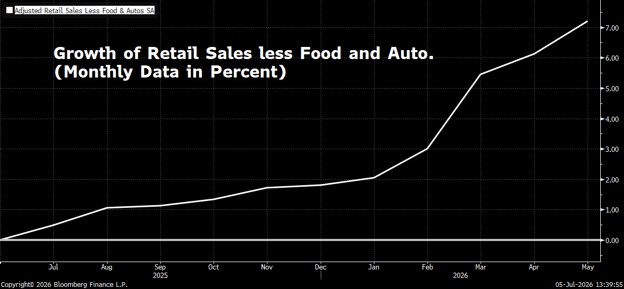

Lower Oil Prices but Higher Chip Prices By Mitchell Anthony July 5, 2026 Overview Wow what a difference a quarter can make! Investors jumped for joy in the second quarter as oil prices plunged and brought down inflationary expectations with it. The war with Iran seemingly has ended and consumers reacted with increased consumption of goods and services. (Figure 1). The economy grew stronger as consumption of AI compute continued to expand and Chip production and related demand has brought most fabs to full capacity. Chip prices have jumped across all areas of production and related devices are feeling the impact. Device producers are no longer able to absorb the higher chip prices and have raised pricing on devices. Apple announced almost a 20% increase in pricing for the iPhone 18. The markets looked past the pricing problems on chips and markets roared upward with domestic equities rising at double-digit rates for the quarter. MACM’s dynamic growth portfolio gained over 20% far surpassing the S&P 500 return of 14%. Large-cap growth beat deep cyclical value names dramatically and tech was the best sector with energy the worst. Bonds were generally losers again. Foreign markets grew at half the rate of American markets. Economic Review Q2 2026 Problems with inflationary expectations that had been dogging investors and keeping the Fed in a hawkish position found some relief. Prices at the pump fell dramatically helping consumers fill the tank more economically. All areas of the energy market found lower prices as the war with Iran came to a halt. Inflation however is still a bit of a problem because demand for AI compute has driven up the price of chips and related devices and all of this is weeping into higher prices for consumer products and Enterprise Products. The Federal Reserve brought a new chairman to the table who has taken on a hawkish tone and vows he will return inflation to 2%, something Chairman Powell was unable to do. Interest rates moved a bit higher in the quarter on the longer end of the curve but the Fed funds rate remained unchanged. The economy seemed to get better in the second quarter. Unemployment fell from 4.4% to 4.2%. Job openings rose and the jolts number which had been hovering around 6600 is now over 7300. Consumer debt continues to be manageable and there is no visible rot in the debt markets. Earnings for the S&P 500 rose an astounding 27% in the second quarter and GDP logged 2.1% quarter over quarter growth. This is a substantial improvement from what we’ve seen over the last few years. It’s actually hard to understand because the economy generally doesn’t do well when housing is not doing well. Both new-home sales and existing home sales are sitting at very modest levels and there is nothing exciting going on with home sales or home construction. Consumer’s wages continue to rise close to the inflation rate or better seemingly underpinning the increased consumption we are seeing in the economy. The industrial sector which was in recession for the last few years began a recovery over six months ago that continues. The demand for industrial products seems to be underpinned by data center buildout with only minor help from housing and durable goods. Financial Market Review The big story in the second quarter was all about American equities and the Nirvana environment that continues to support one of the best equity markets in modern economic times. Growth stocks which had lagged for a few months suddenly roared back into the lead. For the last several years investors have found secular growth companies to be much more favorably positioned than deep cyclical companies. As a result, growth has far outperformed value. (Figure 2). Value stocks have tried to return to favor and investors have bought them several times over the last several years only to throw in the towel and abandoned these speculative bets when the environment failed to support a cyclical rebound in the economy and the deeply cyclical companies that support manufacturing and industrial production. Expectations rose in the quarter for healthcare, Airlines, networking equipment, heavy equipment, and chip production. These were some of the leaders in the equity market last quarter. Expectations fell for software, energy, materials, media, and chip designers. These stocks lagged. Generally domestic equities rose 5 to 20% led by tech and the industrial sector. The magnificent seven was strong again. With interest rates tilting higher and the Fed moving to a more hawkish position bond investors retreated and prices were flat to lower in the quarter. Fixed income has been out-of-favor for quite some time and nothing changed thus far this year. Real estate investment trusts had a reasonably good quarter with returns of 5 to 10%. Bitcoin fell another 10% or more in the quarter adding to its string of losses as investors seem to have lost their interest in this store of value. Economic Outlook The economic outlook for America continues to remain bright. The Economy is well supported fundamentally with relatively low interest rates, manageable inflation, and consumers that have wages that have mostly kept up with inflation. The level of prices is still a problem but consumers seem to be getting accustomed to the higher level of prices and are spending a bit more. The outlook for growth in both earnings and GDP is as good as it’s been in several years. Earnings growth for the S&P 500 is expected to be an astounding 28% this year. The outlook for GDP growth is mixed with substantial differences between economists, market strategists, and the Atlanta Fed, who is ultra-bearish with only a 1.2% forecast. We believe that consumption will remain strong in the major themes of consumption in the globe. This includes artificial intelligence compute capacity, digitization of data, entertainment and leisure, e-commerce, and healthcare. Financial Market Outlook We continue to believe Equities are better positioned than other risks Assets as the Stronger economy pushes rates up further. Without much change seen in the economy with most of the major consumption engine staying on course we suspect the theme of investment in stocks will remain steady as well. It is relatively easy to see rising expectations for chip designers, airlines, hotels, and select areas of software. At the same time some areas of software that are impacted directly by AI will likely stay on a downward path. With the US economy doing better it’s reasonable to think that some of the export engines in Asia and Latin America will do better. Emerging markets will likely continue to perform similar to American markets and maybe better. Most of Europe lacks innovation and leans heavily on deeply cyclical manufacturing, and industrial production. As a result Europe will likely grow slowly and these markets will underperform their American counterparts. Still not the time to become a global stock investor! No real reason to leave America. The move in small-cap stocks that began a year ago is notable (Figure 3) but it is not underpinned by strong economic growth supporting most of these industrial and deeply cyclical areas of the economy. There are selective areas in the small-cap world that are benefiting from AI that are worth investment but they are difficult to value and risky rifle shots. Fixed income looks untimely and treasury rates will probably rise another 20 basis points before the end of the year. We remain optimistic. Figure 1 (Retail Sales). Figure 2 (Comparison of Performance of large Cap Growth Stocks to Large Cap Value Stocks).

Figure 2 (Comparison of Performance of large Cap Growth Stocks to Large Cap Value Stocks).

Figure 3 (Comparison of the performance of Small Cap stocks to Large cap Stocks over last year).

Figure 3 (Comparison of the performance of Small Cap stocks to Large cap Stocks over last year).