Economy Stays Strong but Risk Assets Move Lower Again in Q3

By Mitchell Anthony

October 10, 2022

The US Economy has found a way to avoid recession despite a record rise in interest rates.

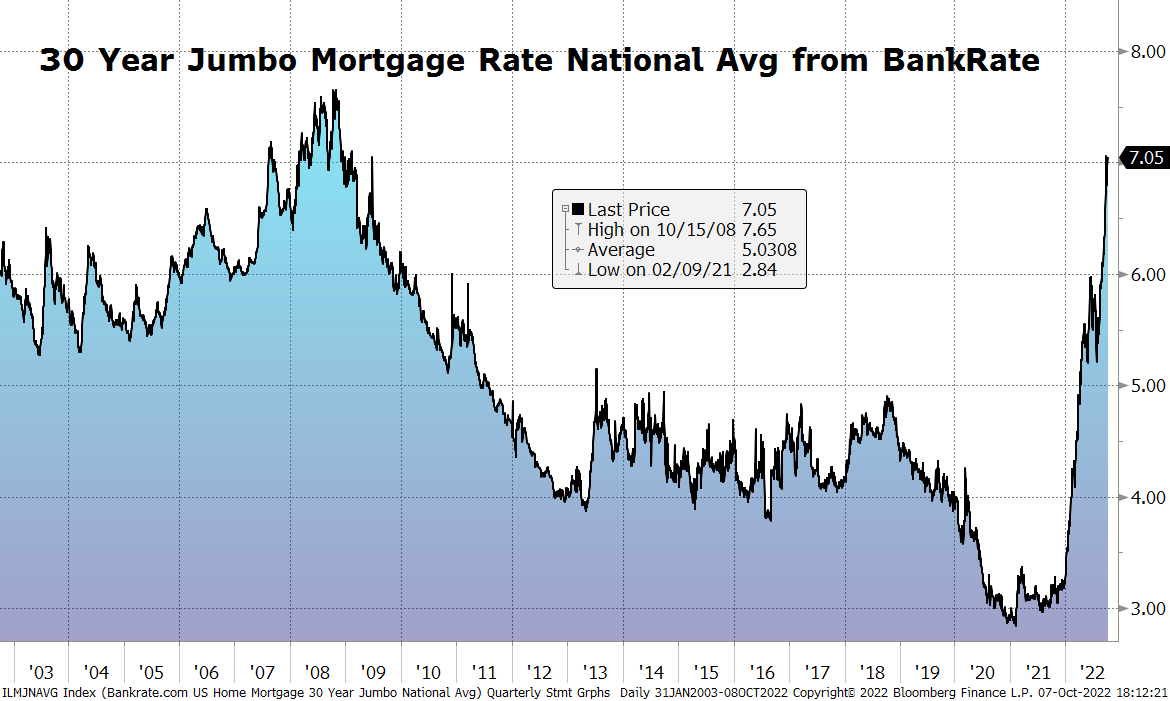

Consumption in the US economy has remained resilient despite a record rise in interest rates and the highest inflation in 40 years. This is somewhat unexplainable but likely tied to the fiscal stimulus that was poured into the US economy in a plentiful manner by the U.S. Congress as it worried about getting the economy back on its feet after Covid. Investors and strategists seemed almost certain that the US economy was headed for recession in the first half of 2022 as the FED began to raise rates aggressively, however after two quarters of negative GDP optimism for economy growth has sprung back to life and the 3rd quarter is expected to be positive with over 2.5% GDP. Actually the US economy was never seemingly in recession despite the negative growth. Unemployment has remained at near record lows and with it came a return to strong consumption. That’s the positive spin, however as we all know inflation is out of control and central bankers are in the position of busting it even if it means busting the values of all risk assets as well as consumption and employment. The Fed has been at work raising rates and investors have been doing it right along with the Fed. Mortgage rates have risen from 2.5 to over 7% currently (figure 1). Surprisingly housing has not busted and consumer spending has continued to grow. Strong Employment seems to be the backbone of the economic resilience. Consumers still have liquidity from Covid stimulus, though it seems to be waning based upon a notable increase in credit usage.

Here good news on economic growth is bad news for our inflation problem as inflation needs to cool rapidly to avoid significantly higher rates and the economic slowdown has not arrived as thought and is truly needed!

Financial Markets react poorly to the sticky inflation.

Investors are clearly bracing for an economic bust and risk assets have declined significantly over the last year as this inflation problem has accelerated. Stocks have declined 20 to 25%, bonds have declined 20 to 35% and REITs are off over 30% as well. The decline in stocks paused in the third quarter as confidence developed that the inflation problem might resolve easily. However that confidence is all but gone as employment trends have stayed shockingly strong. The rally in stocks in July and August ended in September and stocks first fell abruptly but the pace of decline in stocks now is decelerating. The S&P 500 fell 4.9% in the third quarter after declining 16% in the second quarter. MACM’s dynamic growth portfolio fell only 1% in the third quarter after a 17% decline in the second quarter.

Energy and consumer discretionary stocks performed the best in the third quarter with modestly higher returns. Communication services and REITs were the worst performers in the quarter losing double digits.

Fixed income has not been a haven for risk adverse investors. In fact fixed income has performed for the most part substantially worse than equity securities. Intermediate treasuries fell over 10% during each of last 3 quarters for total loss of 36%. Mortgage bonds, Corporates, and Junk bonds all did better than treasuries but still lost low single digits!

The commodity markets which were red hot in 2020 and 21 have turned cold in 2022. Speculators seem to be leaving commodities and now real supply and demand forces are at play supporting these markets. Volatility seems to be waning as these traders fade but for the most part markets have went lower for commodities in general. Year-over-year oil has lost all of its gain and it’s mostly flat with prices of one year ago. Lumber is down 38% year-over-year and likewise copper down 20% and steel down 60%. This decline in commodities has seemingly set the stage for lower prices for durable goods. Gasoline prices nationwide are mostly flat or lower but in California gasoline prices have remained quite high because of refining capacity problems and a shift to a winter blend of gasoline that is required by the state.

Are Yields of Risk Free Assets High Enough to Draw Investor Interest and spark further declines in Stocks, Bonds and Real Estate?

Yields on various fixed income securities have risen significantly this year with two-year treasuries yielding well over 4% and 10 year treasuries yielding 3.8%. Most money market funds are now returning 3% or more ending over two decades of near 0% returns for cash investors.

Are these yields high enough to draw significant investor attention? The answer is probably no. So what level of yield is enough? A historical review makes us believe that the inflection point for a change in asset allocation from risk assets to non-risk assets generally requires a 5% or more absolute return on cash or fixed income, or a 3% real returns.

How high are risk free yields now? Nominal and Real yields on treasuries are still quite low especially considering the level of inflation. Real yields are negative 2% with inflation of 6% and nominal treasury yields are close to 4%. That is probably just not enough to draw investors into fixed income for anything more than a trade. The buy-and-hold investor will generally not accept a return that is less than inflation and under 5% total yield.

The Outlook

This is the most difficult time in history to try to forecast the direction of the economy and the financial markets because of a very benign inflationary environment that has existed for over 50 years. There is no recent data to evaluate on how markets and the economy work through a significant inflation cycle. However one thing is clear either Inflation or the Economy is going to break. There is tremendous resolve by the Federal Reserve to break the back of this inflation and they will not rest until inflation has been re-anchored back at 2%. This is great news for investors as it will cause investors who have left risk assets to return.

The Economy.

The US economy has significant economic momentum from the stimulus that was poured into it in 2020. The Fed has been working hard to mop up over $2 trillion of unneeded stimulus but he has yet to make a dent in this significant pool of cash that was handed out at a very cheap cost or in some cases free to consumers and businesses. Clearly the feds work with higher interest rates are working to break consumption but we just haven’t seen anything significant occur yet. Mortgage rates have climbed over 100% from 2 ½% last year to approximately 7% today. (Figure 1) This has certainly slowed real estate transactions and prices of homes and commercial and industrial property are just starting to begin to break under the load of higher rates. Interest rates now for mortgages are at approximately the same level they were in 2007 just before the housing industry busted wide open in 2009. That was the worst cycle for real estate history has ever seen. It’s unlikely that will repeat but clearly real estate will at best be on a plateau or a steady decline for the next few years.

Inflation.

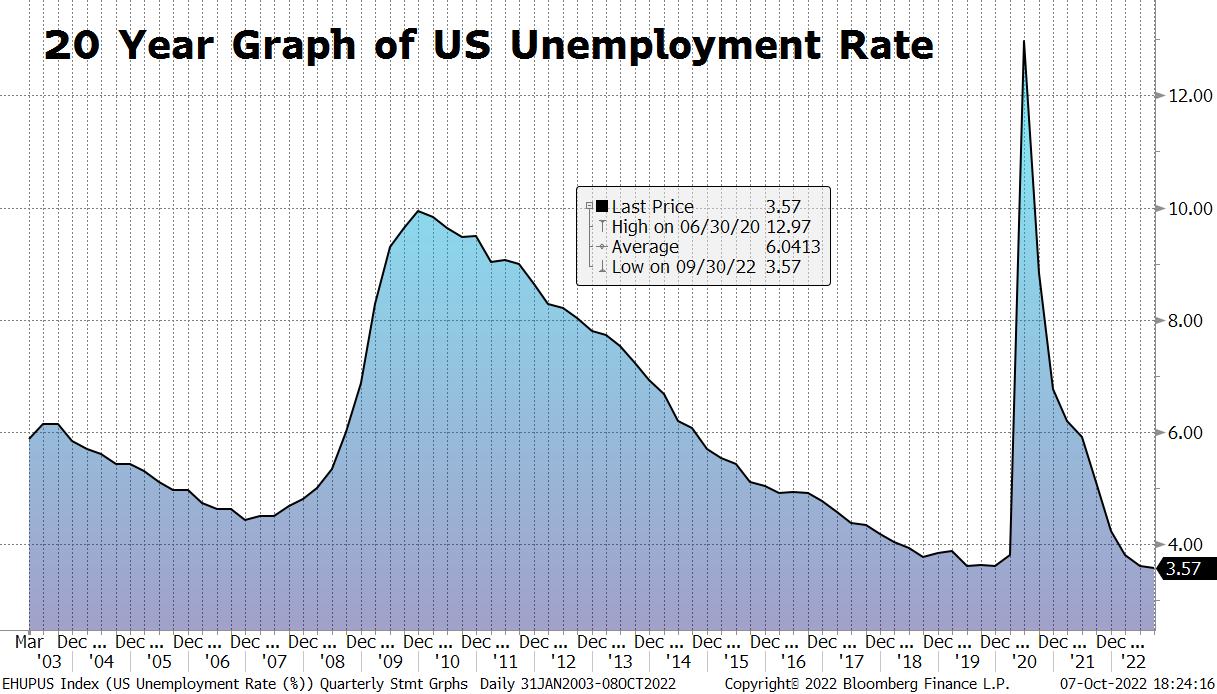

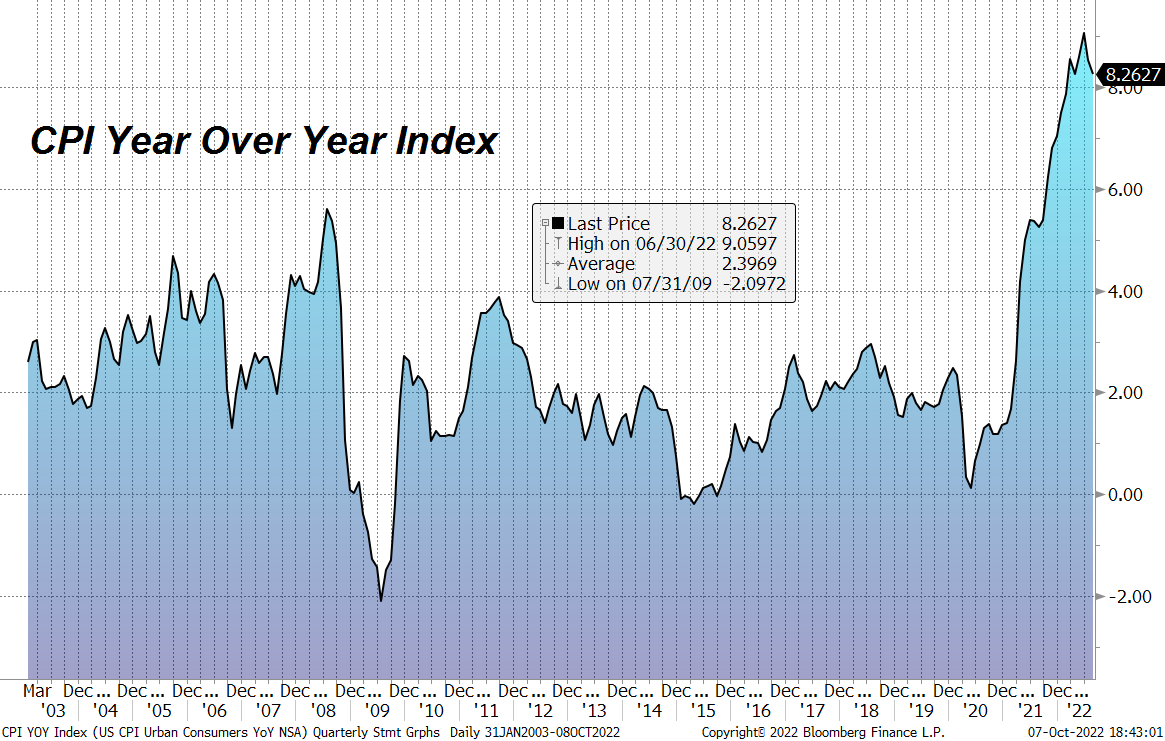

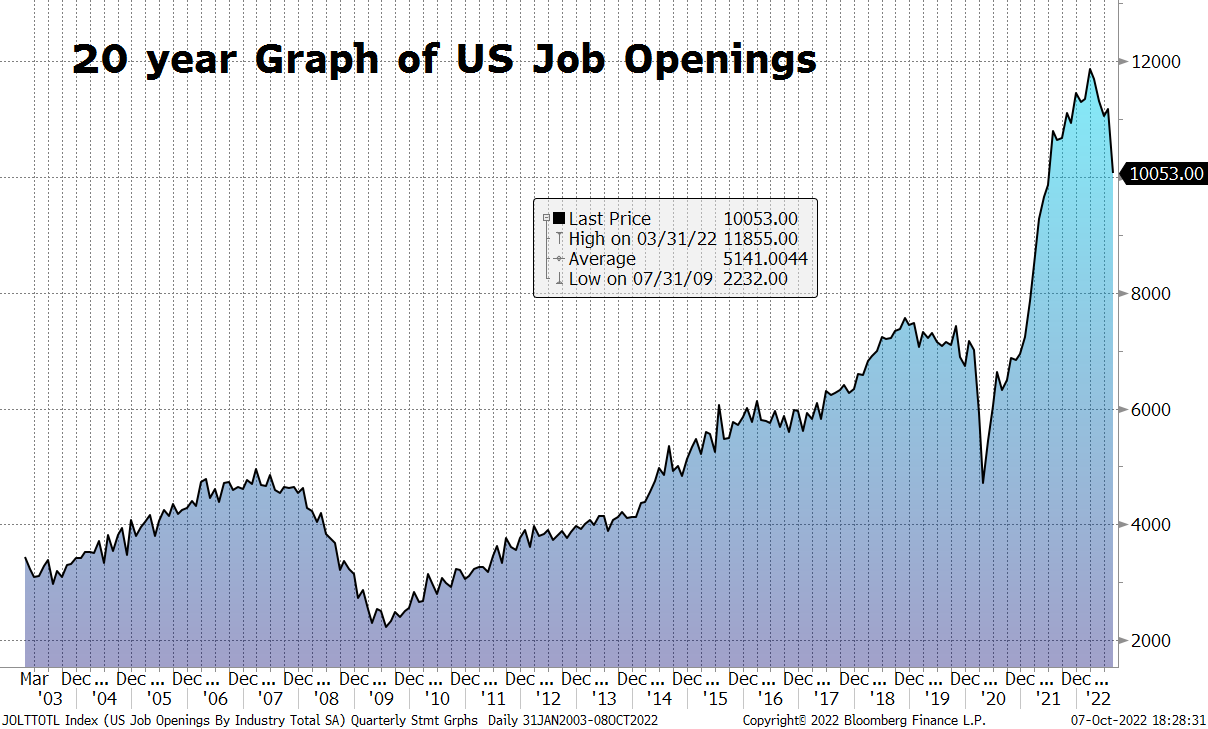

While it seems likely that inflation is on the cusp of a big correction, the decline has not materialized. (Figure 4) Instead the inflation has been sticky particularly in areas like shelter, entertainment, travel, leisure, food and energy. These are all tied closely to consumer spending which is propped up because of strong employment. Some cracks in the employment picture have just started to develop with this weeks JOLTS data point showing fewer jobs than any point in the last year. (Figure 3) Job layoffs are now materializing and we have seen layoffs in the mortgage and credit card processing businesses as well as layoffs and freezes across much of the tech landscape. Both Facebook and Netflix have announced layoffs.

A decline in wealth would certainly change the landscape for inflation and has already begun to play out with over a 60% decline in bitcoin and other crypto currencies along with 20 to 30% declines in stocks and bonds. Wealth drives consumption and as wealth declines consumption should decline with it and prices. We may be on the eve of a bust in home prices that would change the inflationary picture dramatically. Home prices seemingly are already down 5 to 10% from their peak. Some investors are opting to rent homes they don’t need rather than sell them adding to capacity which should in turn reduce shelter costs. Vacancy rates for commercial and industrial property are climbing and we anticipate a significant fall in the value of these areas of real estate. Package delivery and freight companies have reported significant declines in demand for shipping and prices are coming down as a result. Big-box retailers produced far too much last year and are stuck with significant amounts of inventory leading to price cuts on these durable goods.

Countering these trends for lower prices are policies from Congress to keep more stimulus coming to the US consumer. Biden’s decision to forgive thousands of dollars in student debt is inflationary. California is in the midst of handing out stimulus to help consumers pay for gas for their cars. Fiscally there is too much free money in the economy already and the last thing we need is more free money added to the current pile the central bank is trying to mop up.

The Outlook – Markets.

The outlook for the financial markets is still challenging with the inflation storm still overhead. Fixed income markets have been hit directly by the central banks action to raise rates and bond investors have seen the worst year in a decade for intermediate or long-term bond losses.

Fixed income

- Yields likely near a top but 100 basis points higher is possible – to early to buy bonds longer than 2 years.

- Fed seems intent on keeping rates high until inflation breaks, (still not clear exactly what they are looking for on inflation and where the final destination of rates will be.)

Equities

- Earnings yield of stocks is high relative to Bonds creating value and support for current prices.

- American companies perhaps most attractive globally as other countries have worse inflation/energy problems and are not acting as aggressively (in central bank terms) to fix

- Speculative premium is gone in secular growth stocks and they seem to offer good value.

- Leadership likely in areas that will see rising estimates for earnings

- Oil & Gas Producers, Electric vehicles, Healthcare, REITS,

We are optimistic that the markets will survive this storm that is still overhead and believe the current June lows will hold without significant downside from here. Optimism will likely come later this week with the CPI and PPI report. As the inflationary cycle ends both equity and bond markets will make new highs.

Figure 1

Figure 1

Figure 2

Figure 3

Figure 4